Underwriting the Gig Economy: Why Alternative Data is the New Gold Standard

The gig economy is no longer a niche workforce segment. It is now a permanent part of the global labor market. Yet for many traditional consumer lenders, this audience still falls outside standard underwriting models.

Gig workers, from rideshare drivers to freelance consultants, often have strong earning power but limited traditional credit history. Legacy decision engines struggle to recognize this, leading to automatic declines for qualified borrowers.

To reach this growing market, lenders need to move beyond FICO-only decisioning and adopt a more complete data strategy. Alternative credit scoring uses real-time behavioral and financial signals to build a clearer view of repayment risk.

Scale Your Lending

Stop leaving good borrowers behind. Schedule a Technical Deep Dive to see how GDS Link automates alternative data orchestration across your credit stack.

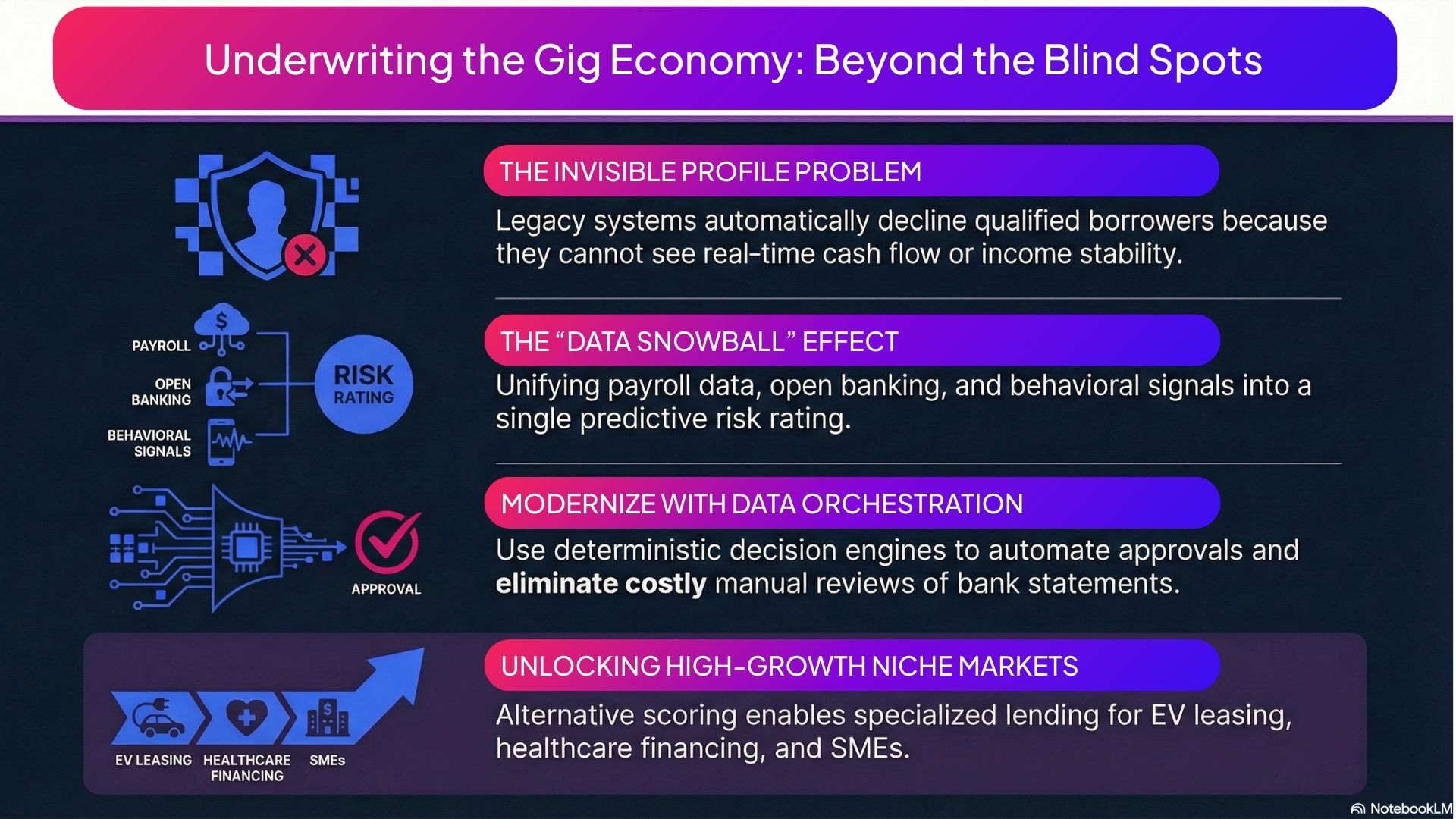

The Invisible Profile Problem

Traditional credit models rely heavily on long-term credit history and W-2 income. Many gig workers simply do not fit this profile.

The result is a large conversion gap. Legitimate applicants are declined because legacy systems cannot see actual cash flow or income stability.

When lenders rely on these outdated metrics, manual review becomes the fallback. Underwriters are forced to comb through bank statements and tax documents to justify exceptions. This process is slow, costly, and difficult to scale.

If your goal is high auto-decisioning rates, your decision engine must evaluate applicants using modern financial data, not just bureau scores.

The Solution: The “Data Snowball” Effect

GDS Link helps lenders unify multiple data sources into a single predictive risk rating.

Instead of relying on static bureau scores, the platform standardizes thousands of credit attributes alongside open banking signals to create a complete borrower profile.

By integrating alternative sources such as real-time payroll data, bank cash flow, and behavioral indicators, lenders gain visibility that traditional systems miss.

All data is normalized across major bureaus, making it easy to change vendors or introduce challenger models without rebuilding your credit policies. This flexibility allows teams to evolve underwriting strategies without engineering delays.

Unlocking High-Growth Niche Markets

Alternative credit scoring is already driving results across high-growth segments:

EV Leasing

Lenders evaluate rideshare drivers using trip volume and earnings history to approve vehicle leases for borrowers with thin credit files but consistent daily income.

Healthcare Financing

Open banking data helps assess real-time ability to pay, enabling point-of-care financing without relying on hard credit pulls.

SME Lending

Small business owners often mix personal and business finances. Orchestrating both data sets provides a clearer view of business performance and repayment capacity.

Download the Roadmap

Ready to modernize your underwriting? Download the Platform Overview to learn how to integrate alternative data in as little as 48 hours.

Conclusion: Efficiency Without Headcount

Expanding into the gig economy does not require hiring more underwriters.

By combining alternative data with a deterministic decision engine, lenders can automate approvals for prime segments and route only complex exceptions to case management. This improves operational efficiency, reduces default risk, and supports audit-ready decisioning.

Is your credit box too small?

Recent articles

Beyond Chatbots: Deploying AI Skills for Sub-Second Underwriting

Read article

The $3.6 Billion Leak: Automating Income Verification in Auto Loan Origination

Read article