The “Invisible” Subprime in Consumer Lending: Detecting BNPL Stacking with Alternative Credit Scoring

Buy Now Pay Later (BNPL) continues to reshape ecommerce and consumer lending. By 2025, BNPL is expected to account for nearly 9% of U.S. ecommerce spend. That growth has created a material blind spot for traditional consumer lending institutions.

A growing share of BNPL activity does not appear on standard credit reports:

- 45% of BNPL originations go to deep subprime consumers

- 63% of BNPL users hold multiple simultaneous loans

- Nearly 1 in 3 borrowers stack BNPL across multiple providers

Because many BNPL providers do not consistently report to bureaus, these obligations remain invisible during underwriting.

This creates the phantom loan problem. Borrowers appear qualified based on bureau data while carrying hidden installment debt that compresses cash flow and increases early default risk.

To protect portfolio performance, consumer lenders must move beyond static credit files and apply alternative credit scoring using real time cash flow markers to evaluate true repayment capacity.

Uncover Hidden Risk

BNPL as the “Canary in the Coal Mine” for Consumer Lending Risk

Although BNPL loans may sit off file, repayment stress shows up quickly in other consumer lending signals.

BNPL users consistently exhibit elevated revolving behavior:

- Average credit card utilization among BNPL borrowers ranges from 60% to 66%

- Non BNPL borrowers average closer to 34%

This utilization spike is an early warning indicator. It often precedes missed payments, balance chasing, and first pay defaults.

Without visibility into BNPL stacking, lenders approve borrowers who appear stable but are already overextended. The result is silent portfolio drift and rising early stage delinquency.

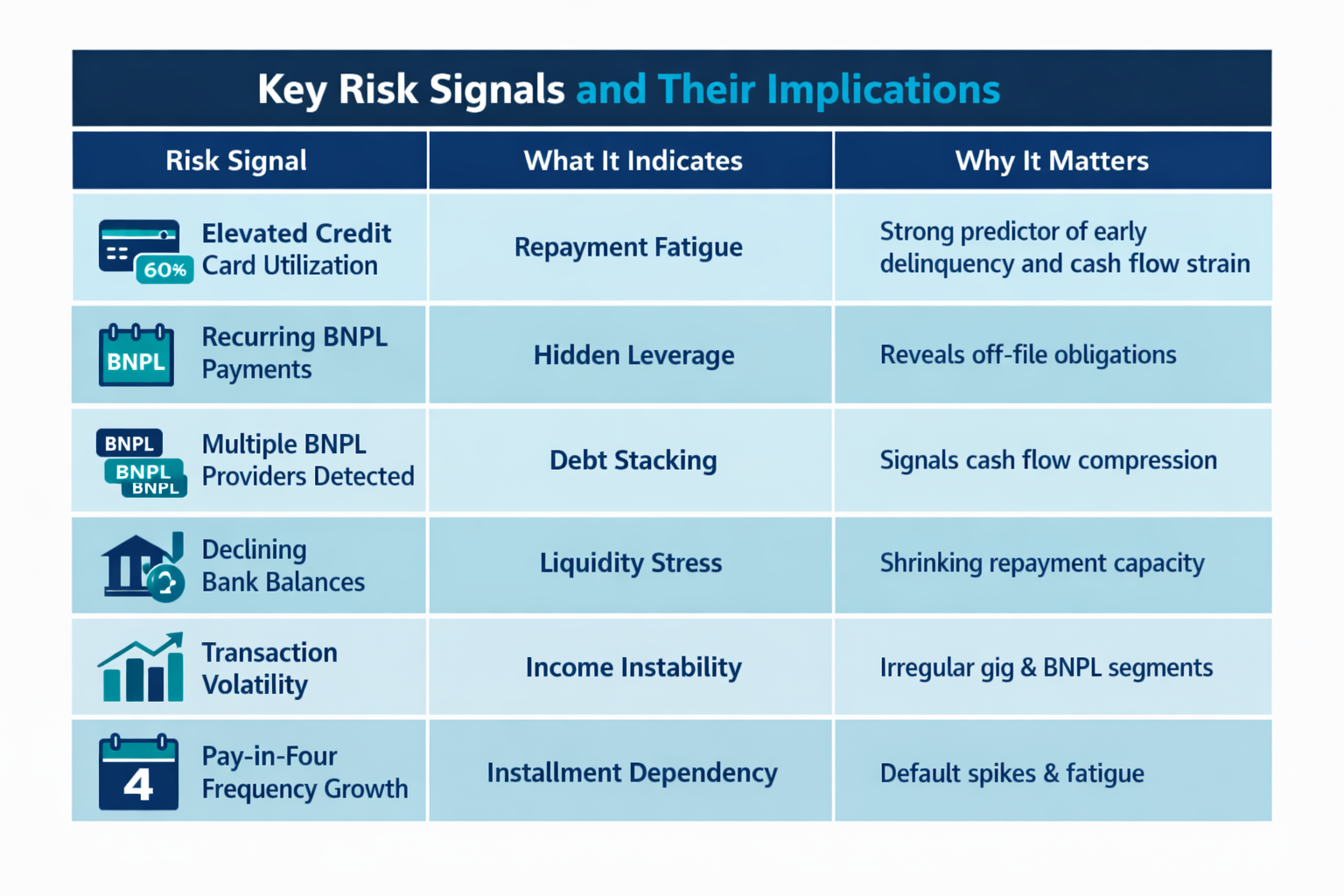

Key Risk Signals for BNPL Exposure in Consumer Lending

Modern alternative credit scoring models look beyond bureau files to detect affordability stress earlier.

Here are the most predictive indicators:

These signals appear weeks or months before traditional credit scores reflect deterioration.

This is where alternative credit scoring provides defensive advantage.

Revealing BNPL Shadow Debt with Alternative Credit Scoring and Permissioned Data

True visibility into borrower leverage requires permissioned transaction data.

Open banking allows lenders to identify recurring BNPL payments directly inside bank histories, even when those obligations never appear on a bureau file.

GDS Link supports this through integrated data orchestration that:

- Ingests 1,000+ open banking attributes tied to income, spending, and payment behavior

- Normalizes cash flow markers alongside 7,000+ standardized consumer lending attributes

- Identifies recurring BNPL installments and stacking patterns before default occurs

This approach converts invisible BNPL exposure into measurable risk and improves affordability assessment for thin file and underbanked borrowers.

Designing Consumer Lending Infrastructure for BNPL Policy Volatility

Consumer lending risk does not change slowly.

Regulatory guidance, BNPL reporting rules, and alternative data availability can shift overnight.

Leading lenders are adopting toggle ready decisioning infrastructure that allows volatile inputs to be enabled or disabled without rebuilding models.

This enables institutions to:

- Maintain dual configurations with and without BNPL or alternative credit signals

- Reduce policy change implementation from months to hours

- Validate strategy updates using Champion Challenger testing on controlled holdout populations

By testing changes on 10 to 20 percent of applications before full rollout, lenders protect portfolio stability while staying compliant.

Alternative Credit Scoring as a Defensive Strategy in Consumer Lending

Invisible debt is no longer an edge case. It is a structural risk driven by BNPL adoption and inconsistent reporting.

BNPL stacking distorts affordability, accelerates defaults, and undermines score only underwriting.

By incorporating alternative credit scoring and real time cash flow markers into automated decisioning, lenders can separate high potential borrowers from overleveraged applicants before losses materialize.

The consumer lenders who win will not approve more blindly.

They will approve with precision.

Is your consumer lending strategy prepared for invisible BNPL exposure? Request your personalized demo and see how GDS Link helps detect hidden leverage with confidence.

Recent articles

5 Things to Look for in a Decisioning Partner When Legacy Systems Are Part of the Equation

Read article

Beyond Chatbots: Deploying AI Skills for Sub-Second Underwriting

Read article